While a home renovation loan and a home equity loan may sound the same, they’re certainly not. The most specific distinction is that home equity loans are backed against collateral and are ideal for big renovation projects. On the other hand, renovation loans are unsecured, are quicker to avail, and are perfect for minor renovations.

Renovation Loans Vs. Home Equity Loans For Home Improvement

Home improvement comes with a hefty price tag, and using your credit card for these expenses could make it even more expensive! But there are cheaper options for this– home renovation loans and home equity loans.

While a home renovation loan and a home equity loan may sound the same, they’re certainly not. The most specific distinction is that home equity loans are backed against collateral and are ideal for big renovation projects. On the other hand, renovation loans are unsecured, are quicker to avail, and are perfect for minor renovations.

Depending on your home improvement needs, both types of loans are ideal options. Read through to learn more about these two options and find which will work best for you.

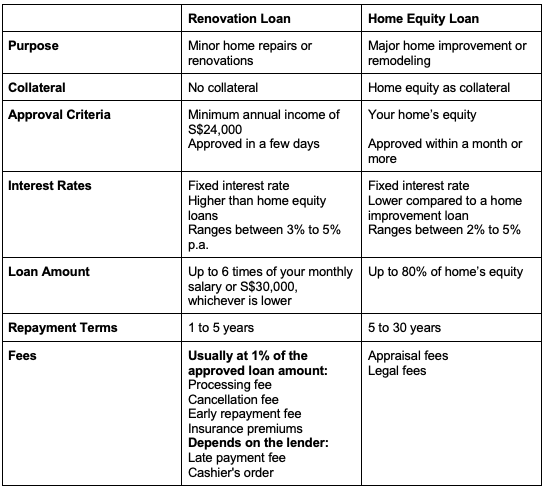

In a Nutshell: Home Renovation Loan vs. Home Equity Loan

Renovation Loan

Renovation loans are unsecured personal loans you can use to finance the renovation of new and existing homes. However, unlike a personal loan, which you can use for any purpose, renovation loans can only be used for home renovation purposes allowed by the bank. Moreover, the lender may also require you to submit a renovation quotation with your loan application.

Pros

● Fixed payments. You will pay the same monthly installment every month, allowing you to budget accordingly.

● Add value to your home. The cosmetic changes and improvements will add to the property’s market value.

Cons

● Low amount. The loan ceiling of S$30,000 may not be enough to cover the full renovation costs.

● Potentially high fees. The interest charges vary from one lender to another and may also be based on your credit history.

● Comes with restrictions. Renovation loans can only be used for approved renovation-related works and can’t be used to buy types of furniture like beds and sofas.

Types of Projects You Can Fund with Renovation Loans

Renovation loans are ideal for major home repair needs. You can use it for the following:

● Repainting and redecoration

● Flooring and tiling

● Electrical installations and wiring work

● Solar panel installations

● Bathroom fittings

Home Equity Loan

A home equity loan is another type of financing you can use for your home renovation projects. This type works as a second mortgage and allows you to borrow against your home’s equity. With a home equity loan, you can borrow a lump sum depending on your home’s appraised value minus your existing mortgage balance.

Pros

● Convert your home’s equity into cash. One major advantage of a home equity loan is to convert your home’s equity into cash and use it to add more value to your home.

● Lower interest rates. Being a secured loan, the interest rates of home equity loans are lower than other lines of credit.

● Flexibility. You may also use funds from a home equity loan for purposes other than home renovation, like consolidating debts, paying for education, starting a business, and more.

Cons

● Property foreclosure. The major downside of a home equity loan is the risk of losing your hard-earned property if you fail to pay your loan.

● Misuse of funds. As you can use the funds for other purposes, it may lead to a cycle of debt and misuse of funds.

Types of Projects You Can Fund with Home Equity Loans

Home equity loans are ideal for significant renovations like:

● Kitchen and bathroom remodeling

● Garden and landscaping projects

● Deck additions

● Major additions like swimming pools or entertainment rooms

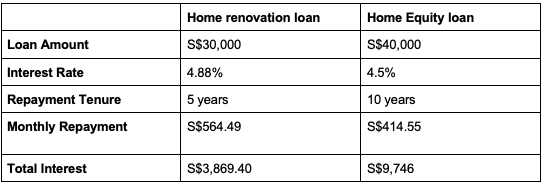

Case study: Jim’s Home Improvement Project

Jim is considering a bathroom and kitchen upgrade estimated to cost S$30,000. With the amount, he can easily choose a home renovation loan that perfectly fits the budget and is easy to obtain. Still, he is also considering a home equity loan as he may want to do other repairs along the way.

He applies for a home renovation loan and a home equity loan with the following details:

Jim chooses the home equity loan due to its lower interest rate and longer repayment term, resulting in lower monthly payments.

The table above shows that the renovation loan has higher monthly repayments. However, this may be ideal for those who want to repay the loan within a shorter period and save on interest costs.

As we can see, both loans are viable options for home improvement financing. Still, borrowers should weigh the differences to choose the option that best fits their financial situation and repayment goals.

Closing

Home improvements are an excellent way to set your property’s sale price soaring. But having that fixer-upper for your home won’t be possible if you have limited cash on hand. Yet, choosing between a renovation loan and a home equity loan lies on you. Make sure you weigh the pros and cons depending on your current situation to pick the right fit.

● Choose a home equity loan if you are up for a significant home upgrade and prefer a longer repayment term.

● Your home’s equity can be your most valuable asset, but you might lose it if you put it up against a home equity loan.

● Choose a renovation loan for small home improvement projects that don’t need much cash and you can repay within a shorter time frame.

Comments